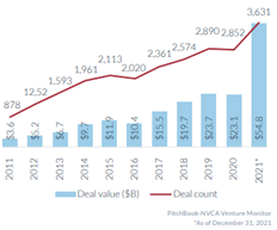

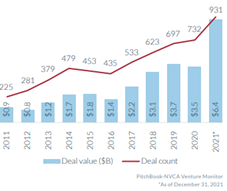

Venture Capital had a record-breaking year in 2021 fueled by US VC backed companies who raised double the amount of 2020 and the highest deal activity level in history. With nearly $800 billion in exits alone in 2021, this was a momentous year for Venture Capital firms, investors, and founders. Taking a deeper dive into 2021, there was an increase in deal activity for companies with at least one female founder as well as overall deal activity for companies with all female founders. An exciting and record-breaking year for VC and female founders. The US VC deal activity for companies with at least one female founder has been increasing throughout the past decade, but in 2021 we saw the highest deal activity and the highest deal value with the value almost 2x of 2020. One of the major reasons for this is because female founders have been steadily increasing year over year and we have seen more female founders making key market decisions in 2021 than we have seen in the past decade. With a higher deal volume count in the beginning half of 2021, VC firms were regaining footing and confidence to deploy capital after a cautionary period due to the pandemic and hoping to reap the benefits of high market prices later in the year.  We also looked into all female founded businesses to see how those numbers matched with the 2021 companies with at least one female founder. With the significant spike in deal count in 2021 for female founded businesses, we anticipate and hope the record-breaking year for 2021 is only the start for the booming US VC deal activity and female founded businesses activity will continue to increase as a percentage of the total deal activity in 2022 and beyond. By: Ryan Peterson, Treya Partners Business Development Manager

0 Comments

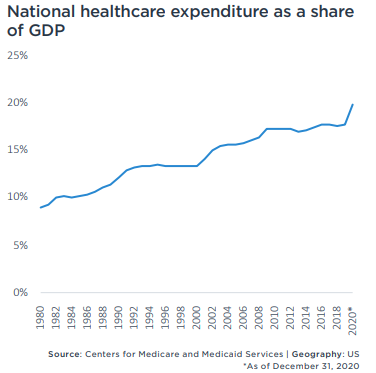

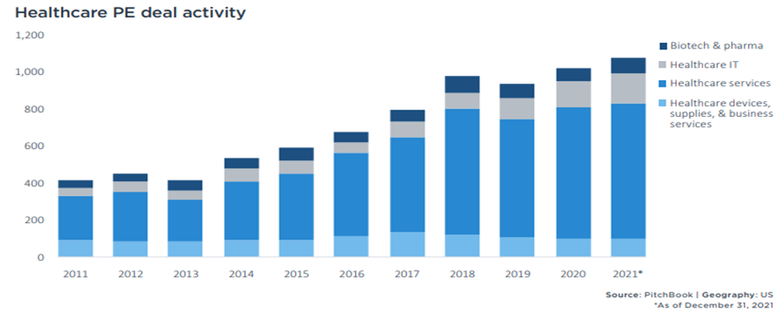

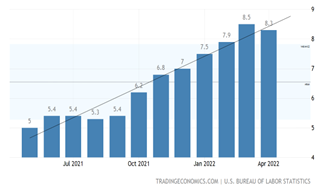

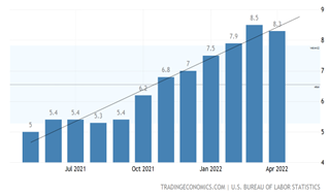

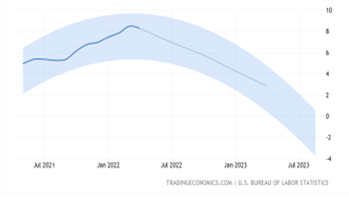

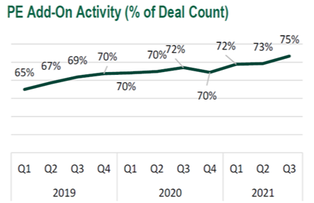

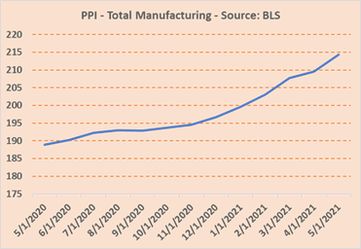

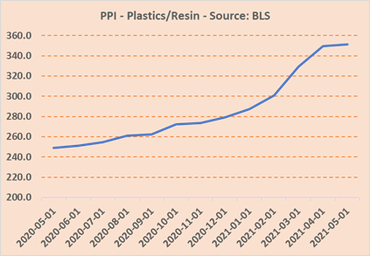

In 2021, there was significant activity by Private Equity firms investing in healthcare companies alongside major industry activity and distributions. We saw an upward spike starting in 2019 in the national healthcare expenditure as a percentage of Gross Domestic Product that topped 20% as of December 31, 2020. There are a few factors shaping the upward trends in the healthcare industry with one of the major factors being the COVID-19 pandemic. The pandemic’s effect on the industry has been both positive and negative. The negative being that at the beginning of the pandemic, hospitals were struggling and costs for COVID-19 safety precautions were rising which made hospitals lose investors and revenue. As a whole, it was estimated that hospitals in the United States were losing $50 billion dollars a month due to COVID-19. Along with the hospitals losing $50 billion dollars a month, inflation took charge on prescriptions and vital over-the-counter medications. There were also minute clinics, primary care, and specialty care institutions that saw loss of revenue due to the patient’s fear of the virus itself. However, the good news was that once vaccines were created in early 2021, we saw an upward revenue trend in hospitals but also the mental health industry, veterinary services, and home care started on that trend as well. Once individuals received vaccinations and felt more comfortable leaving their residences in early 2021, revenues for hospitals increased close to pre-pandemic revenue along with other facets of healthcare increasing theirs. In Private Equity, the number of deals in healthcare has nearly doubled since 2012 from approximately 500 to 1000 per year. COVID-19 was a factor in deal activity in 2021 within Healthcare IT, but through the past decade of deal activity 60% of the deals have been in Healthcare Services. Others sub-sectors include biotech & pharma, healthcare IT, healthcare devices, supplies, and business services. Deal activity in IT and Biotech in healthcare has increased in the past decade as new technology and innovation has taken place. Though it does not match the deal activity of healthcare services, they have remained strong in the past few years. With healthcare devices, we have seen low activity and steady investing within that space. Healthcare Biotech, IT, and devices are going to continue to grow in years to come with more innovative technologies on the horizon.  With the pandemic still present for the foreseeable future along with the rising costs of healthcare and aging population requiring more services and technology, PE firms have strategically invested into the healthcare sector with view of what is needed to prosper in a future healthcare disaster. With hospitals investing in better services, supplies, devices, and technology, firms can have an ease of mind when investing. It will be interesting to see where the healthcare industry goes in 2022. We know that PE firms have an interest in this sector because of the large share it has in the economy, but the industry will need to continue to grow and create better outcomes for patients and providers for firms for future success. By: Ryan Peterson, Treya Partners Business Development Manager ESG (Environmental, Social & Governance) programs have been on the horizon as a commitment for Private Equity firms and portfolio companies for the last several years. However, in the latter half of 2021, we saw more funds launched to invest in sustainability, adjust their investment strategy to invest in companies that source strategically and responsibly for the future as well as invest time and resources in the evaluation and review of ESG programs across their active investments. The private equity and venture capital ESG leaders look to invest in companies that have goals of net-zero emissions, board & employee diversity, and employee & community engagement. Though these are only a few metrics that can be included in ESG commitments, there is a concrete encompassing idea that stakeholders want to invest in responsible companies. When looking at ESG risk factor during the due diligence phase of any investment, a majority of firms have a framework in place to evaluate the key components while at the same time want to do more around ESG in the due diligence process. The minority of PE and VC firms that do not have a plan in place for ESG risk factor during the due diligence process face or will face external pressure from LPs to develop and deploy the process improvement. Additional pressure likely comes from regulatory bodies at the industry level or national level as we have seen in Europe. For the firms that do not have a process in place today, there is certainty that the pressures will build with impact on fundraising, relationship with debt providers, and reputation with operators.  Whether the objective is to target acquisitions that are net-zero companies or to help current investments source quality and more sustainable products & materials, there will be a push for firms to invest in ESG platforms that will be used for reporting and vetting current and future investments, respectively. If the investments do not meet the ESG standards, it is crucial that the investment team or committee clearly understand the areas that fall short, are able to develop high level plan to improve and have confidence in the operator’s ability to execute on the plan. Failure in any of these areas will have a material impact on exit value of the acquired company, return on the current fund and ability to increase size of the next fund. When it comes to implementing ESG programs as the portfolio company level, there are some areas where there are more “ESG friendly” areas to impact and industries that are more capable of being considered environmentally and socially responsible. Other industries like oil and coal have many years before conditions are optimal for ESG standards, but still have an opportunity to develop and execute on an ESG plan to make incremental improvements. Regardless of the industry mix of the portfolio for the Private Equity firm, there are risk factors that come with not constructing an ESG program or minimizing the value of an ESG program. In 2022, the PE firms that want to improve and expand ESG programs and frameworks will need to consider a few areas. One is creating a quality program that covers areas that are common to all holdings with flexibility and customization to meet the needs of a specific industry or to meet the portfolio company where they are. For it to be a quality program, firms need to look at environmental impacts based on specific portfolio company industry. Technology companies need to make improvements in the recycling of IT hardware, reduce power consumption at their data centers, and reduce the carbon footprint of each employee. Compared to manufacturing companies that focus on the sustainability of their suppliers, reduction of carbon emissions at their facilities and programs to offset emissions within their transportation network. The social initiatives programs should be evaluated closely to ensure they align with the organization and the employees. Local and regional initiatives are highly recommended to create direct connectivity between the employee and the initiative. Even though Governance is generally well addressed in the due diligence process by most PE firms, this area should not be taken for granted and will need ongoing reviews and monitoring to comply with the ESG program. Another critical area for a best-in-class ESG program is the quality of data collection and reporting. The deployment of a data collection and reporting process or tool is the heartbeat of the program that keeps everything connected to it alive. Without a process or tool, even the most well thought out and comprehensive program will eventually die out or become so ineffective that all lose interest. Without benchmarking, standardized metrics, reporting on KPI’s and the simple tracking of process within ESG, all aspects of the program are weakened. To build quality metrics, there needs to be fast and easy data collection to ensure both the PE firm and portfolio companies maintain accurate data that tie into the overall ESG initiatives. It will be interesting to see where every industry moves towards when talking about ESG as well as the thresholds for ESG standards when firms decide to invest and approach ESG programs and reporting with active investments. By: Ryan Peterson, Treya Partners Business Development Manager  From a recent article written by the Wall Street Journal, firms have announced nearly $1 trillion ($944.4 billion) worth of deals in the U.S as of month ending September 2021 which include buyout deals as well as exits. This figure is 2.5 times the amount from the same time period in 2020. We will likely see new deal volume and exits increase through 2022 fueled by the current state of cash to deploy for equity investment and low interest rates on debt financing. When alluding to the increased buyout and exit activity in the Private Equity industry, we have also seen add-on’s increasing and as of September 30th, 2021, add-ons are at the highest level in history!  Add-ons accounted for 73.2% of US buyout activity in 2021. The total number of buyouts were 3,845 and of the total buyouts being completed in 2021, an impressive 2,814 were add-on’s leaving 1,031 non-add-on buyouts. At this pace, we can expect the final 2021 numbers to show a record high of buyout deals for the calendar year. We are seeing that add-on activity as a percentage is increasing partly due to Private Equity’s appetite in the past for platform investments that are driving add-on’s today, as well as the competitive environment forcing investors to put capital to work in areas like add-on’s that were not a traditional part of their investment strategy. In the end, it is hard to pinpoint exactly where the ambition comes from for these add-on deals. It is clear that add-ons as a percentage of the total deal volume is trending upward.  Further evidence that 2021 will be a record year is the following deal activity from Q3. The total deal count in Q3 was 2,227 creating the highest deal count in all of 2021. We are currently seeing a widespread distribution of deals in a variety of sectors including materials & resources, IT, healthcare, financial services, and energy. The reasoning behind most of the deals in Q3 being in these sectors could be because of the firm’s interest in more ESG related investments including strategic sourcing in materials, clean energy, and healthcare. With different trends entering the Private Equity space and encouragement from stakeholders to invest in strategic portfolio companies, the deal count is likely to rise in Q4 and in 2022.  With buyouts and add-on activity on the rise, firm’s internal resources to manage and execute on integrations and value creation plans will be stretched. In order to deliver on the investment thesis which may include capturing synergies from add-on’s, firms may need to onboard or expand their 3rd party service provider relationships to squeeze every bit of potential value out of these investments. The level activity combined with the current supply chain and labor constraints place an added burden on the teams and present an opportunity for the right partnerships to accomplish initiatives in areas such as sourcing of materials, transportation, and logistics solutions, along with the low hanging cost reduction opportunities in the portfolio to increase savings and efficiency across the board. With the add-on and buyout activity on the rise, it will be interesting to see where the final Q4 deal volume lands and what key indicators we can extract from 2021 to forecast trends for 2022. By: Ryan Peterson, Treya Partners Business Development Manager   ESG (Environmental, Social and Governance) initiatives within Private Equity have become a crucial asset for the firms and their portfolio companies. Though these initiatives have been around for some time in other industries and public sector, we are currently seeing a gradual implementation of these ESG programs within Private Equity focusing on the firm’s values as well as shaping investment strategies. After attending the PE Innovators in ESG virtual event, I have seen a mindset shift from Private Equity firms showing that investing in companies that are limiting their carbon footprint, growing their diversity and inclusion capacities, and implementing ESG solutions for reporting is becoming essential while maintaining growth within the firm and their portfolio companies. When it comes to implementing these ESG programs, stakeholders have a major impact in contributing to these initiatives. Whether it is investing in ESG platforms or prioritizing programs to promote the ESG vision at a firm or a portfolio company, it all starts with the stakeholders. Including feedback from employees and/or customers in the decisions stakeholders make is critical to create a solid foundation in ESG initiatives across the firm. Our Co-Founder & Partner at Treya Partners, Rahul Ahuja, contributed to a conversation about ESG and the importance of stakeholder involvement which you can watch by via link below. PE Innovators in ESG Speak: ESG Starts with Stakeholders Panel By: Ryan Peterson, Treya Partners Business Development Manager According to a recent article published in the Harvard Business Review, the Private Equity industry is navigating through its mid-life crisis. Per the HBR piece, a recent study found a meaningful drop in average buyout performance of six percentage points between the 10-year annualized return in 1999 and the comparable return in 2019. The challenges that face the industry are two-fold, both financial and operational. We still find ourselves in a seller’s market with multiples remaining at record highs and that, combined with a reduction in effectiveness of traditional PE financial tools (i.e., leverage and price arbitrage), has created an environment for PE where it is more difficult to maintain high performance levels. These financial head winds are being accelerated by operational inhibitors as well. HBR suggests that “Global competition and commoditization make it harder for products to command a premium price, which squeezes margins, and often a business’s easy-to-accomplish cost savings have already been collected by previous owners. A classic PE strategy — integrating small acquisitions into an existing business — still offers revenue growth and other benefits, but its popularity raises the prices of these acquisitions, so returns naturally fall”. These factors and market conditions facing the Private Equity industry have forced firms to evolve in their thinking around value creation and where it can be generated for each of their investments. What we are seeing with many mid-market PE firms is that the traditional model of equipping former CXO’s with Operating Partner titles but deploying them in an advisor capacity is losing favor. More and more firms are creating Portfolio Operations teams comprised of former executives, consultants, and operators. The key difference in the Portfolio Operations model vs. the traditional Operating Partner model is that these folks are required to roll up their sleeves and get busy creating value, prioritizing initiatives, and achieving alignment with portco leadership. There are both specialist and generalist operations models that exist in mid-market PE and these teams are deployed across the portfolio to execute on Value Creation Plans (VCPs). These initiatives can range from ERP deployment to M&A synergy capture, to procurement. All of which are worked on in hopes to increase efficiencies within the investment and ultimately complete value that can no longer be attained through traditional measures mentioned in the first paragraph. At Treya Partners, our work is oftentimes alongside mid-market portfolio operations teams. As portfolio operations practices mature across mid-market private equity, we expect to see a continued shift where teams will be comprised of more generalists who will then bring in trusted 3rd parties to serve as force multipliers on their initiatives. The PE operating model is continuing to evolve not only as to how the team is comprised, but also how they engage with portfolio companies. Working alongside executive teams and finding the right balance between creating value and finding alignment with portfolio company leadership is a major key to success for PE Operations teams. A Kearney study that polled PE backed CEOs was called out some best ways for PE operations teams to engage. Per the Kearney study, “The vast majority of CEOs (nearly 90 percent) think the PE operations team should get involved during the pre-acquisition due diligence phase. The rest want interaction to start as soon as practical after the transaction closes”. This is indicative of a conclusion that we at Treya Partners have drawn in assisting PE operations teams engage with their portfolio companies, assess their spend, and execute where opportunities exist alongside portco leadership. Our conclusion is that the sooner a PE operations team can get engaged and present value to a new investment, the better. It is crucial that value creation teams are engaging during this honeymoon phase where a company is going to be most willing to embrace the ways in which their new private equity ownership can immediately benefit from being a part of their new portfolio. The same Kearney study goes on to illustrate which initiatives portco CXO’s require the most support and where PE Operating Teams tend to deliver it:  Additionally, challenging the status quo and bringing fresh ideas to the table in a collaborative fashion has also shown to be strongly valued by CXO’s:  In our experience, a PE operating team bringing a new portfolio company on to Treya’s leveraged private equity small parcel contract shortly after onboarding has been an effective way to score a quick win and establish a collaborative relationship. Saving a company a few hundred thousand dollars with the stroke of a pen and minimal business disruption goes a long way to establishing credibility for a PE operating team and set the stage for future willingness to engage further at the portco level and leverage more of the value creation tools in the PE firm’s toolbox. The continued maturation of the PE industry, combined with the increased competitiveness we are seeing in the deal markets, is going to force the hand of more and more firms to equip themselves with folks who are exclusively focused on creating value for their investments. It will be exciting to track the evolution of different funds that are different stages of this cycle. I would expect to see most mid-market firms with no dedicated operating teams begin bringing on operations focused individuals in house over the next 5 years. For those firms with existing PE operations teams, the maturation process will consist of continued work within their portfolios which will provide valuable lessons learned. I expect they will also work towards striking the most effective balance between building out in house resources and partnering with 3rd party resources to serve as arms and legs for certain initiatives. This is the function we at Treya Partners serve with most of our Private Equity clients. Most operating teams that we work with have realized they are most valuable and effective when working on high profile initiatives in collaboration with the Investment teams and they lean on trusted 3rd parties for projects that create value and with the right partner, can be repurposed over and over again within the portfolio to drive optimal value. We relish in our role as an extension of PE operating teams and are looking forward to next few years as more firms adopt this model and continue to fine tune the delicate art of PE operations. By Chris Tasiopoulos About the AuthorChris has over 5 years of management consulting, client relationship managment, and business development experience. In his role as Business Development Manager at Treya Partners, Chris is responsible for client relationship managment, Private Equity client cultivation, and development. Chris has led numerous strategic relationships and worked closely alongside both investment and Operations teams at Private Equity firms incluidng Waud Capital, Trive Capital, Trivest Capital, HCI Equity, Greenbriar Equity Group, Heartwood Partners, etc. At the portfolio company level, Chris has worked closely with exectuive leadership to identify cost reduction opportunities and marshalled the Treya deliery team to execute on these opportunities. With significant pressures building, PE firms and Their Portfolio Companies Need to Act Proactively As Recent Supply Chain Distruptions are Creating Inflation  “Good luck finding a rental car in Hawaii! My friend ended up renting a U-Haul on her Hawaiian vacation recently because she couldn’t get a rental car due to the shortage.” These are words we never expected to hear this summer, but have. A series of unrelated recent events – the Covid-19 pandemic, expiration of temporary tariffs relief, the deep freeze in Texas, the Suez Canal blockage, and the Colonial Pipeline hacking incident - have led to a severely disrupted global supply chain – and in turn, supply chain disruptions like these. A significant imbalance between supply and demanding is also fueling inflation. As demand rebounds as pandemic restrictions are lifted, and the American economy feels the effects of the $1.9 trillion stimulus package, supply is constrained due to raw materials shortages and shipping delays. With supply not meeting demand, Producer Price Index (PPI) as measured by different Bureau of Labor Statistics (BLS) indices is significantly higher than twelve months ago. Input cost increases are resulting in both business to business and business to consumer price increases. For instance, US gasoline prices are at a 7 year high, used car prices are up 24% year-over-year, and lumber prices are up a whopping 95% from pandemic lows.  Portfolio Company Impact

Many PE portfolio companies whose revenues were negatively impacted by Covid have seen a healthy bounce back, with business back at close to pre-Covid levels. However, while some of these companies used Covid as an opportunity for some belt tightening, none of them forecasted the level of inflation we are seeing in input pricing. As the rest of 2021 unfolds, this will lead to significant margin erosion, which most companies have not anticipated for, or built into their budgets and financials. Many portfolio companies, as they close out the year, will be looking at significantly worse financials (than current forecasts) if they do not act proactively. How Can Private Equity Firms & Their Portfolio Companies Combat Inflation 1. "Push Back" Against Supplier Cost Increases

2. Pass through Price Increases to Customers (where possible)

3. Utilize Strategic Sourcing

About Treya Partners Treya Partners is a management consulting firm specializing in procurement value creation, strategic sourcing, and spend management advisory services for Private Equity. Treya was established in 2006 by a seasoned group of supply management professionals and has served hundreds of PE-owned companies across a broad range of industry sectors including manufacturing, distribution, retail, financial services, life sciences, healthcare, and technology. Treya delivers meaningful EBITDA improvements from indirect (SG&A) and COGS categories in addition to implementing transformative procurement projects. For further information, visit Treya Partners online at https://www.treyapartners.com. By: Barnali Mishra About the Author Barnali Mishra is a Principal with Treya Partners. Barnali has over 17 years of procurement consulting experience and has delivered high impact procurement and supply chain services to numerous private equity firms and their portfolio companies. Barnali has led and managed strategic sourcing initiatives addressing over forty spend categories and has extensive experience performing spend analysis, opportunity assessments, planning and executing competitive solicitations, conducting complex category strategic sourcing, and performing fact-based supplier negotiations. Barnali holds both a BA and an MA from Stanford University. Barnali resides in San Francisco and enjoys traveling the world with her husband and daughter. A Key Missing Ingredient in the Private Equity Due Diligence Process in Today's Market  The Backdrop: It's a Sellers Market with Dry Powder at a High Within the world of private equity, dry powder has reached a new high of $1.4 trillion, having grown 17% annually since 2015. In turn, there are a lot of investors and not enough deals to be found. It is a seller’s market, and GPs are having a tough time justifying doing deals at today’s high multiples of 12 – 17x. Concurrently, in our experience at Treya Partners, we find very few Private Equity (PE) firms formally incorporate procurement value creation into their due diligence and underwriting process. Sometimes contract risk mitigation (e.g., in the case of Carve Outs) is considered, but rarely are procurement cost savings reliably estimated and underwritten into the deal thesis. With purchase multiples being high and a fiercely competitive market for deals, GPs need to recognize the competitive edge that can be gained from reliably estimating and underwriting procurement value creation into the deal.  Why to Incorporate Procurement into the Due Diligence Process

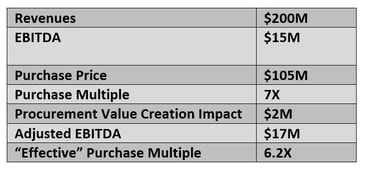

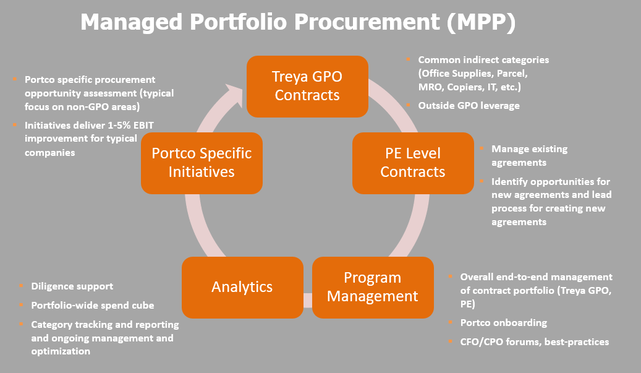

We at Treya recommend that PE firms begin including Procurement Value Creation as a critical element of their due diligence strategy. Not only can procurement optimization improve cash flow right away, it can set the stage for future acquisitions, and ultimately, maximize value at exit. More importantly, if there is a significant procurement opportunity, it can lead to a much lower “effective” purchase multiple for the deal, allowing for a higher purchase price and ultimately in a higher close rate. How & When to Incorporate Procurement into Due Diligence Incorporating procurement value into your firm’s due diligence is not difficult – an Accounts Payable (AP) spend analysis will give you a directional idea of the procurement savings opportunity available. Include procurement up front in your data collection efforts - request a year’s worth of AP data and know that high-level spend by vendor data will suffice if that is all that is readily available. Potential procurement savings and associated value can then be estimated from this data. In addition to SG&A expenses, COGS can also be targeted to significantly enhance the opportunity. A confidence level should be built into savings estimates to mitigate execution risk. Done right, this process will create a significant competitive edge for winning deals. Sources: Pitchbook, Private Equity Wire By: Barnali Mishra Mishra is a Principal with Treya Partners. Barnali has over 17 years of procurement consulting experience and has delivered high impact procurement and supply chain services to numerous private equity firms and their portfolio companies. Barnali has led and managed strategic sourcing initiatives addressing over forty spend categories and has extensive experience performing spend analysis, opportunity assessments, planning and executing competitive solicitations, conducting complex category strategic sourcing, and performing fact-based supplier negotiations. Barnali holds both a BA and an MA from Stanford University. Barnali resides in San Francisco and enjoys traveling the world with her husband and daughter. The 5 Most Important Considerations in Launching a Successful Private Equity Procurement Program4/19/2021  At Treya Partners, our focus is primarily on cost reduction initiatives for Mid-Market Private Equity firms and their portfolio companies. As you would expect, we have conversations with mid-market firms on a daily basis regarding value creation. These conversations provide us with unique insights across a wide range of Private Equity firms regarding how Value Creation is addressed today. When we ask about value creation, there is one common theme that we keep hearing: procurement has historically been a blind spot at the PE level. There are multiple challenges that have contributed to procurement being under leveraged as a value creation lever for mid-market firms. Those include a lack of resources, changing priorities, perceived value, shifting responsibilities for team members, and turnover at firms. To combat these challenges, we’ve developed our Managed Portfolio Procurement (MPP) program, which addresses 5 key considerations and provides portfolio companies with a world class procurement offering. Here is a breakdown of those 5 focus areas: 1. Is there clear visiblity into the portolio's spend base? The ability to execute on cost reduction opportunities within a portfolio is only possible if there is clear visibility into the spend base for each portfolio company. It is critical that Accounts Payable (AP) data is collected and categorized on an annual basis for each company within a PE portfolio. Simple AP data analytics will go a long way in understanding where the strategic procurement opportunities exist both at the portfolio and cross-portfolio levels. Building out and maintaining a cross-portfolio spend cube is step one in realizing meaningful procurement value creation outcomes. 2. Is the strategy for low hanging fruit too simple? Interestingly, one of the biggest inhibitors of PE firms that keep them from being able to properly address procurement has been the prevalence of Group Purchasing Organizations (GPOs) in Private Equity. Don’t get us wrong, GPOs for common indirect spend categories such as small parcel, office supplies, and car rental are vital to a holistic procurement program and are part of our toolkit. However, it is all too common for PE firms to roll out GPO contracts to their portfolio companies, consider procurement to be “addressed,” and move on to the next priority, leaving millions of dollars on the table for their portfolio companies. GPOs work for portfolio companies with small to medium size spend in select categories, but once spend in a category exceeds a certain spend level, “off-the-shelf” GPO pricing is rarely the most competitive. 3. Does a strategy exist for portfolio company specific engagements to garner a higher return? The most meaningful procurement impact and EBIT relief will come from strategic portfolio company specific procurement optimization projects. These engagements will use the AP data analytics mentioned above to identify multiple spend categories at a portfolio company that can be addressed through strategic sourcing. Some common reasons why significant strategic procurement opportunities exist at mid-market PE backed companies are a lack of in-house category expertise, fragmented purchasing, a lack of unit level data, and a lack of procurement resources. The ability to identify and execute on these cost reduction opportunities at the portfolio company level in a rapid fashion (3-6 months) creates excitement amongst both the executive teams at portcos and PEdeal teams. 4. Does the program enable and develop procurement leaders across the portfolio? Introducing procurement knowledge and expertise to specific portfolio company is certainly useful, but being able to effectively share and transfer knowledge across the portfolio and educate multiple companies on procurement best practices is an additional layer of value that a best-in-class PE procurement program can provide. Providing the portfolio with access to CFO forums, procurement panel discussions, and SME presentations will help to maximize the utilization of procurement best practices. 5. Can spend be leveraged across the portfolio in certain categories? When reviewing a portfolio wide spend cube comprised of AP spend data from each portfolio company, common vendors and spend categories should emerge. This will be even more apparent if the PE firm’s investment focus is sector driven. There are a number of spend categories where there is a significant opportunity to leverage spend cross portfolio and use the portfolio’s collective purchasing power to negotiate favorable discount and rebate structures with best-in-class vendors. Treya’s MPP program is a holistic five-pronged program that creates a strong procurement foundation for our private equity clients by addressing each of the above areas. Our approach was developed through years of experience working alongside mid-market PE deal and ops teams and implements a program that can rapidly create meaningful EBIT impact while withstanding the headwinds of a fluid and constantly changing PE environment.  By Chris TasiopoulosChris Tasiopoulos is a Business Development Manager with Treya Partners. Based in Boston, MA, Chris supports Treya Partner's private equity clients in several key markets.

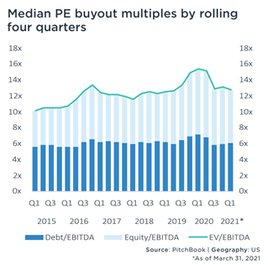

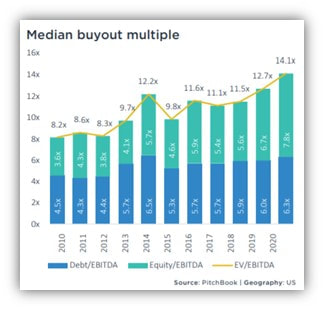

The coronavirus pandemic has not slowed private equity firms from putting their capital to work. Deal activity may have been down from March to April 2020, but deal volume was able to rebound by the fourth quarter of 2020, with deal counts and deal values reaching 10-year quarter highs. Deal multiples have also recovered from early 2020, with the median buy out multiple now at 14.1 (see chart 1). Historically, large, economically disruptive events like the "Great Recession" (2008 – 2010) have had a noticeable impact on private equity portfolio companies' holding periods. Specifically, investments made just before the recession, at peak valuations, were held longer. Chart 2 illustrates the increase in holding periods, peaking at 5.6 years in 2014. These acquisitions required longer holding periods to realize respectable returns. Consequently, median holding periods elongated. From 2014 – 2018, median holding periods for PE portfolio company exits showed a slight-but-steady downward trend, then leveled off just below five years. The coronavirus' extreme economic impact is expected to increase the median holding period as private equity firms delay exits, just like they did in the last recession.  Almost without exception, PE firms will be looking to carefully manage their portfolios and create value during these extended hold periods in the wake of the pandemic (Jones, 2020). Procurement represents an often-untapped opportunity for value creation for many PE firms and their portfolio companies. Many PE firms are behind the curve on managing procurement. Given that operational value creation can account for up to 50% of some funds' internal rates of return (IRR), procurement should be a strategic consideration at the fund level. Optimizing procurement can help PE firms and their operating companies reap the rewards and reduce portfolio risk.

Treya Partners helps our private equity clients leverage advanced procurement capabilities portfolio-wide; this represents a competitive differentiator. Whether your objectives are EBITDA improvements, budgetary cost savings, organizational or business process improvements, or procurement capability development, we provide the right mix of services, best practices, and expertise to deliver results. Our procurement programs are a significant value creation lever for our clients in what remains a highly volatile climate. By Steven DelCarlino, Manager, Treya Partners About the Author Steven DelCarlino leads client engagements and project teams for Treya Partner’s private equity clients and their portfolio companies. With over 15 years of experience working directly with corporations, international businesses, and private equity portfolio companies on strategic sourcing projects, Steven brings a diverse knowledge of spend categories and project management experience. Steven and his team provide a rigorous fact-driven analysis that accounts for the total cost of ownership, service needs, and long-standing supplier relationships for each engagement. Steven has managed sourcing projects in the logistics, packaging, raw materials, finished goods, facilities services, MRO, IT, and wireless sectors, among others. Before joining Treya Partners, Steven was a Manager with GEP Worldwide, a global provider of strategy, software, and managed services to procurement and supply chain organizations. Steven also led the procurement and supply chain offering at CMF Associates (now CBIZ Private Equity Advisory), a financial and operational solutions provider to private equity firms and their portfolio companies. Steven holds a Bachelor of Business Administration from Temple University and is an MBA candidate at the Kettering University School of Management; Steven also has a Supply Chain Management Certification from Villanova University. References: Jones, A. (2020, May 07). Private equity portfolio company holding Periods – Updated. Retrieved February 25, 2021, from https://blog.privateequityinfo.com/index.php/2020/05/07/private-equity-portfolio-company-holding-periods-updated-4/ US PE Breakdown. (2021, January 11). Retrieved February 25, 2021, from https://files.pitchbook.com/website/files/pdf/2020_Annual_US_PE_Breakdown.pdf |