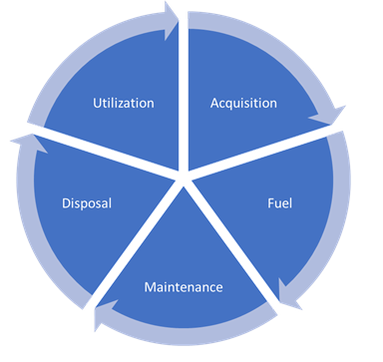

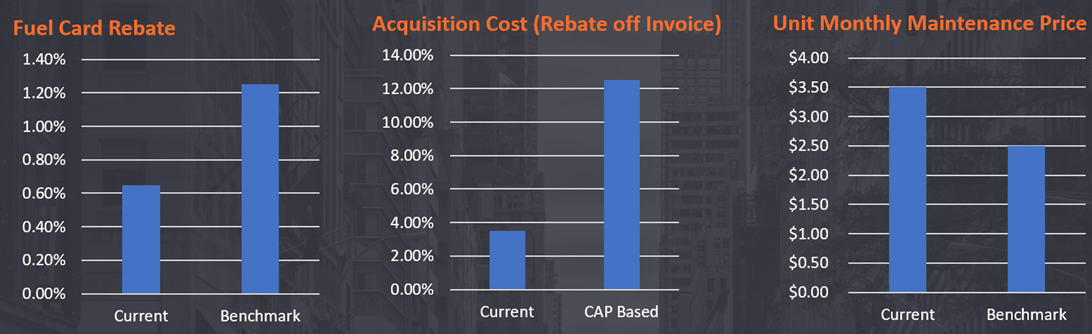

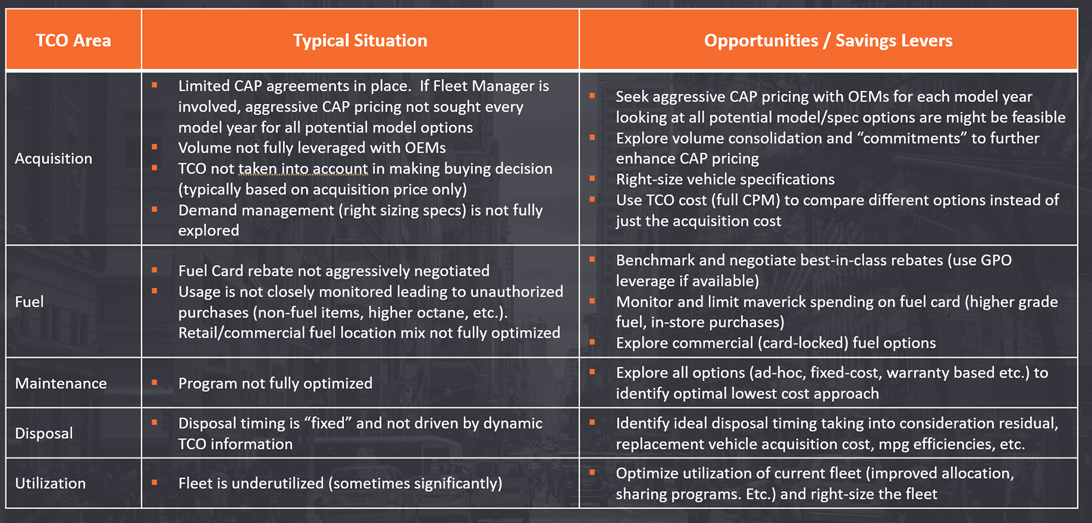

Numerous Private Equity (PE) portfolio companies, especially in distribution and services sectors, utilize fleet vehicles as part of their distribution and operations. Typically, these companies use a Fleet Management company to oversee all aspects of their fleet operations. However, Fleet Management companies do not always take a comprehensive approach to helping these companies optimally assess and manage their fleet costs, resulting in a detrimental impact on EBITDA. Treya recommends a holistic, Total Cost of Ownership (TCO) approach underpinned by detailed pricing, usage and benchmark data, to identity and optimize key cost drivers for fleet ownership and maintenance. This approach typically results in a 8-12% overall cost reduction, improved utilization and improved fleet operating metrics. A TCO approach is critical to understanding and optimizing the total cost of owning and maintaining a fleet. This involves managing each aspect of the life-cycle cost in detail including costs related to acquisition, fuel costs, maintenance costs, disposal value, and overall utilization. Companies should identify current costs and practices in each of these areas and compare those against best-in-class practices, and cost and operating metrics for similarly sized fleets. A quick benchmarking exercise can reveal key gaps in the existing program and key opportunities for improvement. In addition to benchmarking of current costs and operating metrics, companies should also assess and evaluate current practices in each of the TCO components and identify gaps. The TCO Table at the bottom of the article depicts key savings levers that should be thoroughly evaluated in each TCO area. For example, when acquiring new vehicles most companies look at comparing only the acquisition price, whereas if they looked at comparing overall TCO costs (looking at fuel and operating costs, and residual value at the end of the useful operating life) it might lead them to acquire a different vehicle.  Frequently, vehicles with a lower acquisition price (or CAP rebate from the manufacturer) are not necessarily the lowest TCO vehicles. Companies should also look at current maintenance practices and institute best-in-class practices for fleet maintenance to help them reduce maintenance costs and improve fleet uptime. Most companies tend to hold on to vehicles well past their optimal hold times as they are fully depreciated. Companies should do a detailed analysis of overall holding cost and comparison against a comparable new vehicle taking into consideration typically greater fuel efficiencies and residual values. Finally, companies should look to periodically assess overall fleet utilization and seek to ensure that it stays above a minimum threshold.  About Treya Partners

Treya Partners is a management consulting firm specializing in procurement value creation, strategic sourcing, and spend management advisory services for Private Equity. Treya was established in 2006 by a seasoned group of supply management professionals and has served hundreds of PE-owned companies across a broad range of industry sectors including manufacturing, distribution, retail, financial services, life sciences, healthcare, and technology. Treya delivers meaningful EBITDA improvements from indirect (SG&A) and COGS categories in addition to implementing transformative procurement projects. For further information, visit Treya Partners online at https://www.treyapartners.com.

3 Comments

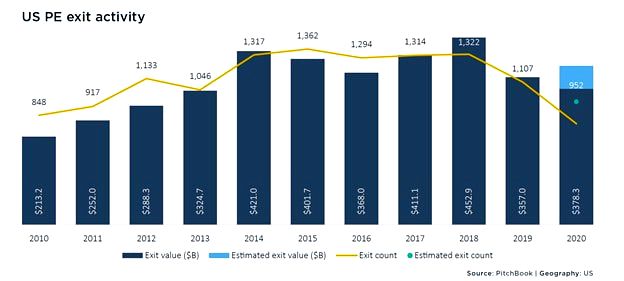

All steps of the Private Equity (PE) investment process are critical from early-stage due diligence to the final exit. After years of executing on the investment thesis including process improvements, product pricing optimization, cost reduction, talent management, add-on’s, tuck-in’s and excercising other value creation levers, a poorly planned or executed exit can make the difference between a great deal and a good deal. To unpack the value pre-exit procurement optimization can create, it is helpful to understand 2020 PE exit statistics: 2020 Private Equity Exit Activity Highlights

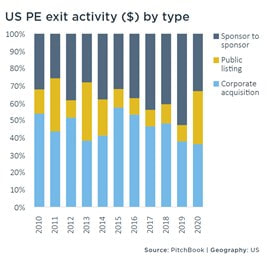

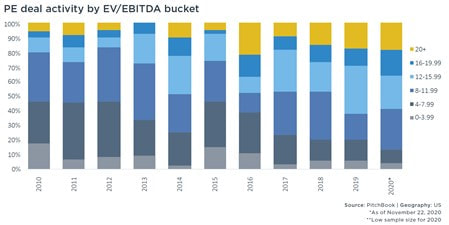

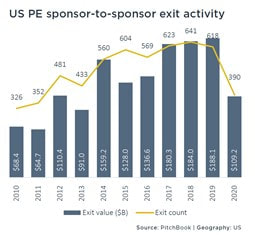

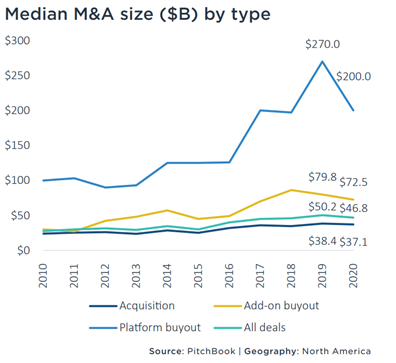

2020 PE Exit Details  Total PE exit value increased from $357.0 billion to $378.3 billion despite the decrease in the number of exits  2021 forecasts indicate a high level of activity with some sources predicting 20% of buyouts will be priced above 20x EBITDA. The graph predicts a YOY increase in buyouts at 20x+. Price multiples in the public markets have carried into private markets. The S&P 500 now trades at a Cyclically Adjusted Price-to-Earnings (CAPE) ratio of 34.77, up from 34.52 last month and up from 30.73 one year ago. This is a change of 0.70% from last month and 13.3% from one year ago. In the private market, the median multiple for buyouts was 12.7x through Q3 2020 which is a record high. Although the average multiple is being driven up by larger technology buyouts that are well above the 12.7x EBITDA level, the majority of exits in 2020 were in the 12x to 20x+ range and the same is expected to be true in 2021   A noticeable trend is the decline of sponsor-to-sponsor exits from 2019 to 2020. 390 out of 952 exits (41%) were sponsor in 2020, while 618 of 1107 exits (56%) were sponsor-to-sponsor in 2019. Although overall exists in 2020 declined from 2019, the percentage decline in sponsor-to-sponsor exits was significant. Pre-Exit Procurement Value Creation The majority of owners struggle to create value past the initial one to three years of the holding period, during which the primary value levers are typically pulled included procurement process improvement, upgrade of talent to support strategic sourcing, and running competitive processes to drive out costs on indirect spend and CoGS. And as the multiples get higher, so does the bar for a successful exit that is taking advantage of all potential pre-exit value creation opportunities. One of the mostly widely underutilized pre-exit value creation levers is procurement. Using the 2020 average of 12.7x EBITDA as the valuation, a narrowly focused and strategically executed procurement improvement initative will typically delivery $10M to $25M in enterprise value for mid-market portfolio companies with increasingly higher returns as the addressable spend increases. At the beginning of the holding period, management is highly engaged and excited to kick-off the value creation process. The management team spearheads large transformation programs, systems upgrades and integrations, reductions in overhead expenses, and commercial improvements in areas such as pricing. In the years that follow, focus shifts to maintenance and M&A activity. The change often results in less focus on further sharpening of the pencil. Management becomes board. As management becomes distracted at the back end of the holding period, swift and targeted procurement value creation engagements can energize the team and produce meaningful impact. Results are dependent on several criteria: Criteria for a Successful Engagement #1 – Management has meaningful equity stake in the company: Equity owners quickly calculate the EBITDA impact of a cost reduction project to valuation and then to their bank accounts. The direct connection is much more immediate than early hold period projections. #2 - Proper Evaluation of Spend to Address: Spend addressed through procurement improvement activities must bring material improvement to EBITDA and create hard dollar savings to be included in Quality of Earnings (QofE) #3 – Adequate Time to Deliver & Document : At least 4 months is required to deliver and document savings during a targeted pre-exit procurement improvement initiative Steps to Maximize Procurement Value Pre-Exit Step 1: Perform an Accounts Payable spend analysis 18 months before the intended time of exit Step 2: Identify 3-5 spend categories or vendors with highest potential for cost reductions Step 3: Identify of sub-set of categories/vendors with lower cost reduction potential to leave on the table as potential value creation opportunities for the buyer Step 4: Determine combination of 3rd party and internal resources to execute on cost reduction efforts, which can include a mix of incumbent supplier negotiations, competitive bidding processes, and GPO utilization Step 5: Complete an ‘outside-in’ assessment of the savings opportunity for each category Step 6: Develop a category by category approach with timeline to execute Step 7: Execute Step 8: Document results for Quality of Earnings. Example of Treya Partners Enterprise Value Creation Results  Treya Partner's Accelerate Program

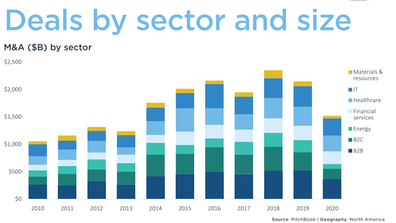

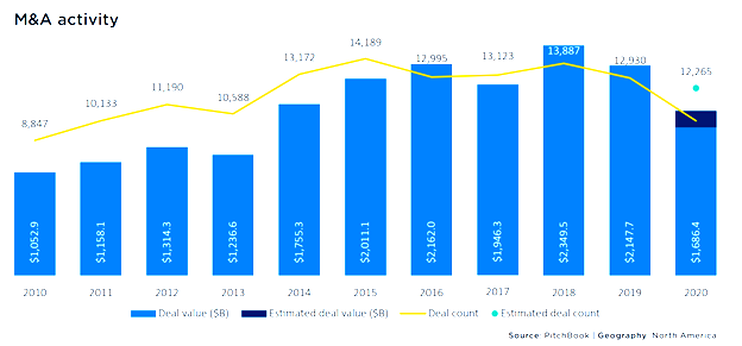

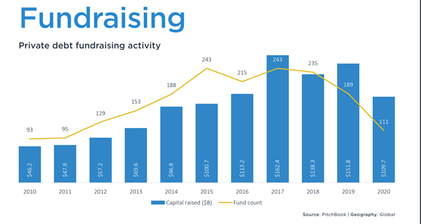

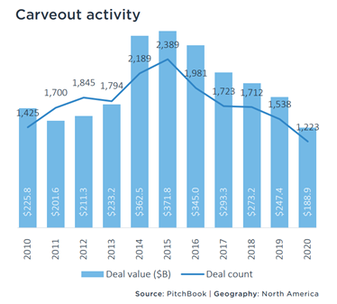

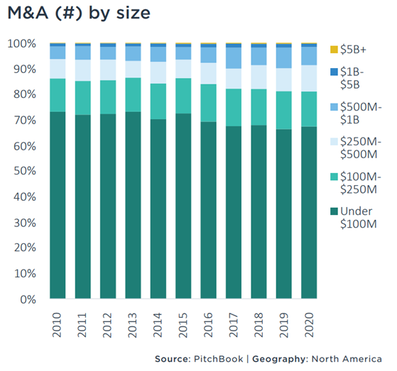

Treya Partners is a management consulting firm specializing in procurement value creation, strategic sourcing, and spend management advisory services for Private Equity. Treya offers a broad range of value creation programs including Managed Portfolio Procurement (MPP), Procurement Transformation, and most recently, it’s pre-exit offering, Accelerate. Accelerate is a “SWAT team” approach to pre-exit procurement value creation designed to deliver maximum value in an abbreviated project timeframe for a seller while developing a procurement value creation roadmap for potential buyers. Treya was established in 2006 by a seasoned group of supply management professionals and has served hundreds of PE-owned companies across a broad range of industry sectors including manufacturing, distribution, retail, financial services, life sciences, healthcare, and technology. Treya delivers meaningful EBITDA improvements for both indirect (SG&A) and COGS spend categories in addition to implementing transformative procurement improvement projects. For further information, visit Treya Partners online at https://www.treyapartners.com.  What We Saw in 2020 - 2020 was a year that spanned the activity spectrum in Private Equity. While PE firms entered the year looking to ride the momentum generated in 2019 both on the deal and fundraising front, things came to a screeching halt with the onset of a global pandemic. In Q2 we saw stillness followed by a significant period of uncertainty. Most firms shifted to an all hands on-deck defensive strategy to help their negatively impacted portfolio companies in any way they could. However, the Private Equity industry did not sit back idly and let that become the narrative for all of 2020. By Q3, the initial Covid shock had worn off and activity picked up across the industry. The summer and autumn saw an uptick in activity as PE firms adjusted to a limited travel Covid era existence. Now, in Q1 2021, the industry finds itself looking to ride the unexpected momentum that the second half of 2020 provided. The IT, Healthcare, and B2B sectors claimed the majority of 2020 deals, measured in dollars. As illustrated in the graphic below, those three sectors dominated deal flow in 2020, while the B2C and Energy sectors took a significant step backwards. The graphic below is representative of the momentum that was halted by Covid in the spring of 2020, and then picked back up in the fall. Despite a global pandemic, M&A activity only declined by 5% by number of deals between 2019 to 2020:  What can be expected across the Private Equity landscape in 2021? Deal Flow Will Be Strong  First, we firmly expect the flurry of deal activity to continue through the first half of 2021. With the rollout of Covid vaccines, it seems the most uncertain times are behind us. One glaring data point to support this thesis is the $1.7 Trillion in Dry Powder that the Private Equity industry was carrying into 2021. Capital raised nearly peaked in 2019. That fundraising flurry has surely contributed to the glut of dry powder that exists today, as the Fundraising graphic to the left illustrates. This deployable capital can be expected to be put to work early and often this year, due in part to the backlog of deal related diligence activity in 2020. With much less Covid-related uncertainty now, we expect more deals close as a direct result of the resumption of diligence activity in Q3 and Q4 of 2020. Deal flow in 2021 will also be supported by a likely increase in corporate carveouts. Many large companies have been dealt a significant blow by the pandemic and a significant number of those companies are continuing to feel the pain, over 11 months since the first shutdowns. While they are still struggling to find their footing early in the new year, Private Equity investors have been patiently sitting on $1.7 Trillion in dry powder. Carveout activity has been on a steady decline since 2015. The market is poised for a potential off-trend uptick in carveouts in 2021 and it will be interesting to keep an eye on this in the months ahead. The combination of excess dry powder and large public companies licking their Covid wounds can bode well for opportunistic Private Equity firms looking to close carveout deals as large public companies, especially those struggling, consider all options, including the sale of non-core business units.  Add Ons Will Be Popular Now that we have established the rationale for anticipating a deal heavy year, the question then becomes “What type of deals will tell the story of 2021 in Private Equity?” The Private Equity industry seems aligned on the expectation that Add-On deals will be the most common in 2021. In a recent survey of Private Equity professionals conducted by ACG and sponsored by advisory firm Dixon Hughes Goodman, more than 60% of respondents said they expect add-ons to take center stage. If the back half of 2020 is any indication of what the Private Equity landscape is going to look like during and post-Covid, it is worth noting that according to Pitchbook data, add-on deals accounted for 73% of Private Equity buyouts in Q3 2020, the highest number on record. This trend also leads us to believe that Average Deal Size in terms of dollars will remain consistent with the prior decade, with deals under $250M accounting for over 80% of total M&A activity each year.  Founders Will Be Seeking Investments The propensity towards deal making in 2021 will not just be unilateral with Private Equity firms looking to deploy a glut of dry powder. Family and founder-owned businesses will surely be re-evaluating their openness to sale this year. Even those fortunate enough to survive 2020 with little to no negative impact will still likely have their eyes and ears open as PE firms come knocking. Baby Boomers are in a position where they may want to finally cash in if the right opportunity presents itself. One third of the US population is either close to, or over, the age of 60. Witnessing the fallout from the pandemic and leading their companies through the storm may very well be the final challenge that leads founders to decide that the now is the time to either sell or assist with a management led leveraged buyout. The combination of this baby boomer population aging and the very real risk of them losing their life’s work due to a global pandemic very much out of their control should incentivize founders who managed through 2020 to cut a deal.  2021 Will Be a Busy Year for Private Equity, and Treya Partners is Poised to Support Cost Reduction Efforts for New Deals

The newswire in the Private Equity industry will be hot throughout this year and firms will be ready for the action. Coming off a year filled with uncertainty to a degree many have never seen, PE firms are battle tested and ready to take lessons learned and use them to be as opportunistic as possible in 2021. Focus on operational synergies and integration will be top of mind for fund managers and they will be making sure they have the resources and tools in place to optimize their buy and build strategies. At Treya Partners, we are prepared to be heavily involved in the deals our Private Equity clients close this year and we will be supporting them through cost reduction and procurement optimization efforts so their teams can focus on the next deal to be had in this opportunistic market. About Treya Partners Treya Partners is a management consulting firm specializing in procurement value creation, strategic sourcing, and spend management advisory services for Private Equity. Treya was established in 2006 by a seasoned group of supply management professionals and has served hundreds of PE-owed companies across a broad range of industry sectors including manufacturing, distribution, retail, financial services, life sciences, healthcare, and technology. Treya delivers meaningful EBITDA improvements from indirect (SG&A) and CoGS categories in addition to implementing transformative procurement projects. For further information, visit Treya Partners online at https://www.treyapartners.com. Each year small parcel carriers institute a General Rate Increase (GRI). Given the impacts of Covid on carrier network capacity and the additional capacity burden on the less profitable residential network, 2021 will bring significant GRI increases. For example, FedEx has already announced a general rate increase for 2021 of 4.9% to 5.9% on many services, beginning January 4, 2021. The increase applies to FedEx’s Air and International, Ground, SmartPost, and Freight customers. Accessorial fees will also not go untouched. FedEx will make changes and additions to close to 40 accessorials, fees, and surcharges. The impact on individual shippers will vary greatly depending on package characteristics, shipment type, and ship to locations with large package shippers realizing the highest increase. In addition to the rate increase, FedEx will also institute a 6% late payment fee. As carriers experience an increase in e-commerce residential shipments for over-sized items, additional handling charges may also have a larger impact on a company’s total transportation spend. For example, effective January 18th, 20201, FedEx’s new trigger for additional handling dimensions is 105” combined length plus girth (length and girth = length + 2*height + 2*width). The impact of the added volume to the carriers ground network is evident in UPS Q3 earnings. UPS’s quarterly profit beat expectations, but shares dropped 5.5% as investors scrutinized the drop in margin due to the pandemic. Highlights of the Q3 UPS earnings:

Ending a challenging year of from the pandemic, with a higher than expected peak holiday surcharge is continuing to stress the carrier networks. But what does that mean for 2021? Here are 3 tips to consider as you close out the year of the pandemic and ring in 2021. 1. Develop dynamic models to forecast shipment costs with consideration of standard GRI, volume increases/deceases, accessorial fees, minimum charges and zone increases. Examine the models to determine options for mode shifting, packaging changes, and other areas to minimize cost per package increases. The increases will NOT have the same cost per package impact for all shippers. For example, a low weight e-commerce ground shipper on FedEx will have 6%+ increase for the 1-5lb packages. 2. Re-examine your distribution center locations. Shippers with one coastal distribution center will a national customer base will see larger increases due to longer zones than their competitors with regional distribution centers. Again, modeling the financial and operational impact of an additional distribution center or centers arms you and your team with the data needed to make informed decisions. 3. Evaluate your shipping options and incentives at checkout. Many B2C companies during the pandemic provide additional incentives for online orders picked up a store locations or central locations. There are many different options for shippers to explore.  If you have additional questions about potential cost increases, Treya can assist with modeling and comprehensive analysis of your transportation, accessorial fees and surcharges. In addition to current rate analysis and modeling, we can identify potential cost mitigation options. For Private Equity owned companies, we also offer additional options to manage parcel costs via our leveraged volume rates. Click HERE for additional information on the program.

|